Steel’s 2100 Transition Starts With The Denominator, Not Hydrogen

China’s construction slowdown, scrap growth, cement decline, and mass timber matter more to steel’s future than another round of green-steel hype.

Steel is usually introduced as one of the hard cases for climate action. That is fair, up to a point. The world makes roughly 1.9 billion tons of crude steel a year, and most of it still comes from blast furnaces and basic oxygen furnaces that use iron ore, coal, limestone, and some scrap. Steel is everywhere. Buildings, bridges, vehicles, ships, pipelines, rails, wind turbines, transformers, ports, warehouses, appliances, factories, rebar, beams, sheet, plate, and a very large amount of industrial equipment all have steel running through them.

That scale makes it tempting to start with the technology race. Hydrogen direct reduced iron. Molten oxide electrolysis. Flash ironmaking. Biomethane direct reduction. Carbon capture on blast furnaces. Green iron exports. Low-carbon premiums. First-of-a-kind plants. Government grants. Strategic partnerships. Memoranda of understanding, because apparently no industrial transition is complete without several hundred pages of warm prose and no operating data.

But steel’s transition does not start with hydrogen. It starts with the denominator, which is a less glamorous word and a much better guide to reality. The first question is how much steel the world will actually need, by decade, as China’s infrastructure buildout slows, construction intensity changes, cement demand falls, mass timber scales in some building categories, existing steel stock returns as scrap, and mature electric arc furnace production expands. Only after that do we know how much new iron remains to be made.

That is the frame this Transition Pathway Review uses. It is not a “green steel technology options” article. It is a 2100 steel pathway review, asking how steel demand, scrap, new iron, emissions, and regional strategy change over time.

This is not a new subject for me. In 2023, I worked through steel as a major climate problem with proven tools, then built a 2100 steel demand and technology projection and an accompanying view of how steel’s outsized carbon emissions would shrink as the production mix shifted. I also tested whether wind turbines and solar panels would create a steel constraint, and the answer was clearly no. In parallel, the broader industrial heat work kept pointing to the same conclusion: much of industrial decarbonization is about electricity, not molecules.

The 2025 update changed the emphasis. After a structural steel expert challenged some of my earlier assumptions, I reassessed steel through the lens of falling cement use and China’s slowing construction sector. That reassessment pulled steel, cement, mass timber, scrap, and regional industrial strategy into one transition pathway. The result is a more optimistic steel transition than most heavy-industry narratives imply, but not because a single hero technology wins. Steel can decarbonize because the system is already partly circular, because electric arc furnace steelmaking is mature, because clean electricity is expanding, because demand is probably less heroic than conventional forecasts assume, and because the remaining new-iron problem may be smaller than the green-steel sales decks prefer.

The denominator changed

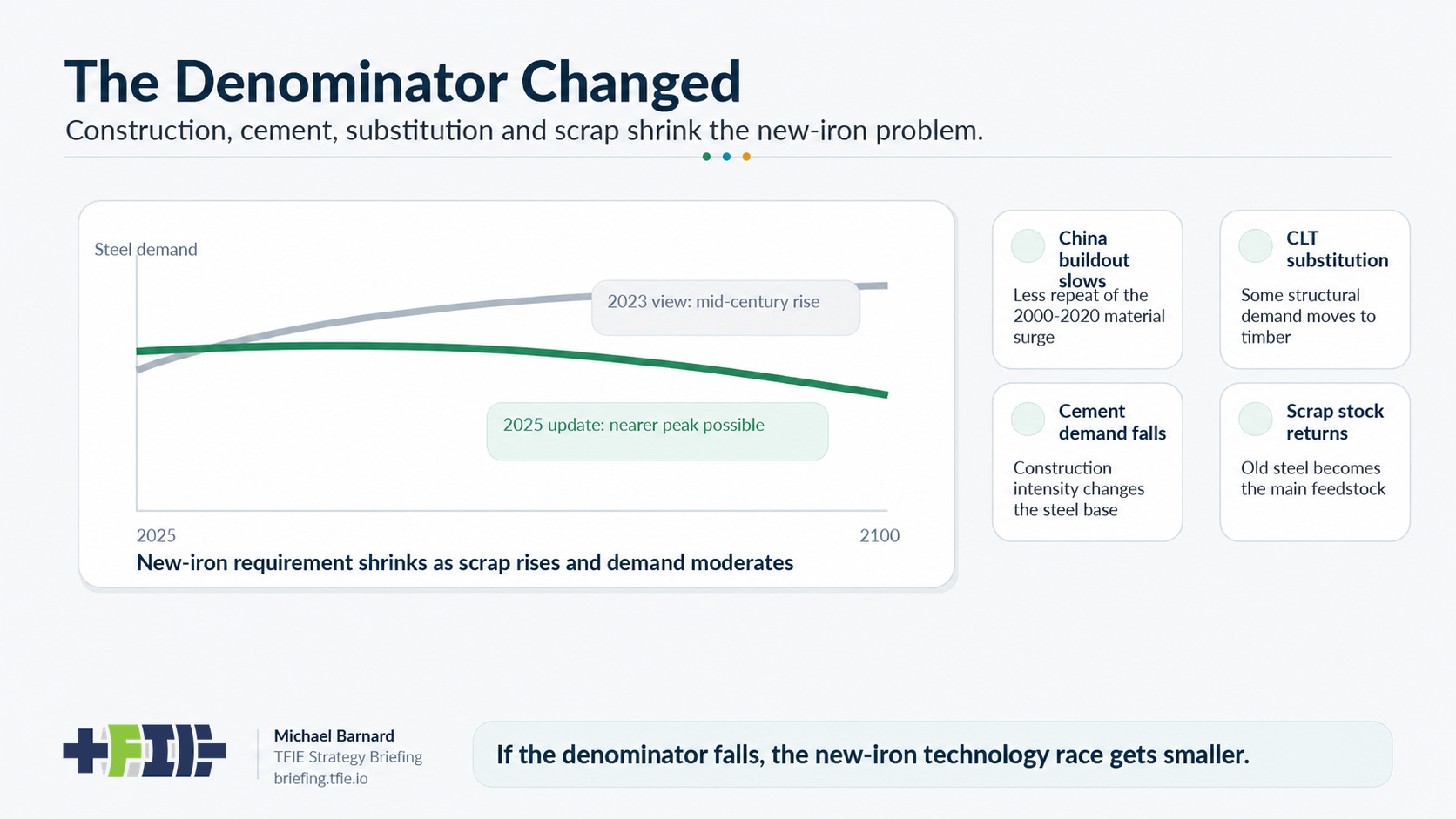

In 2023, my long-range steel projection through 2100 assumed that steel demand would rise into the middle of the century, peak around 2060, and then flatten. The production mix changed sharply over the century, with scrap and electric arc furnaces doing more work, blast furnaces fading, and new iron shrinking as a share of supply. It was already a more practical decarbonization pathway than the hydrogen-everywhere story, but it still assumed continued steel demand growth for decades.

The 2025 update changed the denominator because China, cement, construction systems, and scrap all changed the shape of the question. China’s 2000 to 2020 construction surge was one of the largest material demand events in human history. Repeating that curve globally is a bad assumption. India, Southeast Asia, Africa, and other growth regions will build a great deal, but they are unlikely to recreate China’s exact steel and cement intensity, at China’s speed, with China’s specific urbanization, property, infrastructure, and industrial policy pattern.

Cement matters because steel and cement are coupled through buildings and infrastructure. My work on cement displacement and decarbonization through 2100 already pointed to a lower-material-intensity construction future. The later piece on the levers that reduce cement use reinforced the same logic. When construction systems change, both material curves change. If less concrete is poured, less rebar and structural steel may be needed in some applications. If more construction shifts toward cross-laminated timber and other engineered wood systems, some structural steel demand shifts as well. Not all of it. Steel is not going away. But the denominator changes.

Mass timber is part of that shift. I have argued that Canada has a timber moment if it wants housing, jobs, and climate benefits aligned, and that CLT displacement makes steel and cement decarbonization more realistic. That does not mean mass timber eats steel. It means mass timber, lower-carbon cement, design efficiency, and better material use all narrow the steel demand range.

Scrap matters most over time because steel is not a fuel. It is a long-lived material stock. Old steel returns. The timing is imperfect and the quality challenges are real, but end-of-life steel from vehicles, buildings, infrastructure, appliances, machinery, pipelines, and industrial systems becomes feedstock. My earlier observation that US pipelines contain years of US steel demand was partly a fossil infrastructure point, but it was also a scrap denominator point. The steel already exists. A lot of it will come back.

That is why a 2100 steel pathway cannot be a point forecast frozen in amber. It has to be tested by decade. In 2025 to 2030, the question is whether steel demand has peaked or paused. In 2030 to 2040, it is whether scrap, electric arc furnaces, clean electricity, and procurement form a real market signal. In 2040 to 2050, it is whether the scrap wave is large and clean enough to reduce primary iron sharply. In 2050 to 2060, it is whether legacy blast furnace assets are finally exiting. From 2060 to 2100, it is whether steel is mostly a circular stock-management system with a smaller residual new-iron requirement.

What counts as progress

Steel’s public narrative still overcounts activity. A grant is not a market. A pilot is not fleet replacement. A hydrogen direct reduced iron announcement is not a durable steelmaking strategy. A carbon capture retrofit on a blast furnace is not automatically decarbonization. An orderbook is not always bankable demand. A memorandum of understanding is not steel, although it is certainly evidence that someone has a communications budget.

Real progress looks different. Blast furnaces retire. Electric arc furnace capacity rises and runs at high utilization. Scrap collection, sorting, and quality management improve. Clean electricity is contracted for real production, not just claimed on paper. Steel buyers accept and specify lower-carbon steel where it matters. Green iron and hot briquetted iron trade develops where ore, ports, power, and industrial capability align. First-of-a-kind new-iron routes become commercial plants with qualified product, not just nice diagrams. Construction systems reduce material intensity, and procurement standards and embodied-carbon rules begin shifting demand.

That last point is important because steel decarbonization is not only a production story. Demand-side changes count. If construction uses less material for the same service, that is progress. If building systems substitute mass timber where it is structurally and economically appropriate, that is progress. If infrastructure design avoids overbuilding, that is progress. If existing steel is recovered and recycled with better quality control, that is progress. Steel is not decarbonized only at the furnace. It is decarbonized through the whole material system.

The mature route is already industrial reality

Electric arc furnaces are not speculative. They are not a lab curiosity waiting for a benevolent program officer. They are a mature steelmaking route that already dominates production in some markets, especially the United States. The American Iron and Steel Institute says electric arc furnaces account for over 70% of US steel production. Worldsteel’s World Steel in Figures 2025 shows the global picture is much less electric, with the blast furnace and basic oxygen furnace route still dominant, but that is the point. The electric route is proven, and the global share has room to grow.

Electric arc furnaces melt scrap, direct reduced iron, pig iron, or other metallic inputs using electricity. As grids decarbonize, the emissions intensity of electric arc furnace steel falls with them. That does not mean electric arc furnaces solve everything. That would be the same lazy thinking as assuming hydrogen solves everything, just with a different logo.

Scrap has quality issues. Copper and other residual elements matter. High-grade flat products can require cleaner inputs. Some regions have young steel stocks and not enough returning scrap. Some steel demand growth still requires new iron. Electric arc furnaces need reliable, affordable electricity, along with supply chains, logistics, operators, and customers. But they are already industrial reality, and that changes the transition logic. The central question is not whether electric steelmaking can work. It is how far it can expand, how clean the electricity becomes, how well scrap quality is managed, and how much new iron is required to supplement it.

Hydrogen direct reduced iron works technically. Iron ore can be reduced with hydrogen instead of carbon monoxide from coal or fossil gas, and the resulting iron can be melted in an electric arc furnace. With clean hydrogen and clean electricity, the emissions can be low. None of that is magic. It is chemistry and industrial engineering.

The problem is the comparator. Hydrogen direct reduced iron is not competing only with a coal blast furnace. It is competing with lower steel demand, more scrap, electric arc furnaces, clean electricity, better scrap processing, regional green iron trade, electrochemical new-iron routes, and material substitution. It is also competing with the delivered cost and operational complexity of its own fuel chain.

Hydrogen has to be made, compressed or otherwise conditioned, stored, transported, delivered, and used at high reliability. It needs a lot of clean electricity before the steel plant ever sees a molecule. It introduces a dedicated fuel chain into an industrial process that can often be served more directly by electricity and scrap. For some sites with unusually cheap clean electricity, strong policy support, suitable ore, firm offtake, and integrated infrastructure, hydrogen direct reduced iron may be valid. That makes it niche-valid, not universal.

My 2023 update to hydrogen demand through 2100 still treated steel as one of the few credible growth areas for hydrogen. The later steel reassessment narrowed that considerably. By 2025, after testing multiple new-iron routes, I argued directly that hydrogen would not win the zero-carbon steel race. That was not because hydrogen cannot reduce iron. It was because the delivered economics and the system comparator had moved against it.

Public verdict

The public verdict is that steel’s transition is progressing, with medium confidence. The mature route is scrap plus electric arc furnaces plus clean electricity. The hard residual problem is new iron. That problem is real, but smaller than the common hydrogen framing implies.

Steel can decarbonize faster than most heavy-industry narratives imply, but not because one heroic technology replaces every blast furnace. The main pathway is demand moderation, scrap, electric arc furnaces, clean electricity, and a smaller contest over new iron. That still leaves hard work. The world needs better scrap systems, more clean electricity, industrial policy that rewards real emissions reductions, procurement rules that recognize embodied carbon, and new-iron routes that survive contact with commercial reality. But the direction is not mysterious. Steel’s transition is a denominator problem before it is a technology race.

Below the paywall is the professional layer of the review: the comparator test that explains why hydrogen DRI narrows rather than dominates, decade-by-decade evidence triggers through 2100, regional strategy implications, the final pathway scorecard, and decision tests for steelmakers, miners, policymakers, investors, and buyers. The public argument is here. The paid section is the reusable intelligence layer, the part designed to be revisited as new evidence changes the curve.