Hydrogen Buses Are A Procurement Risk Premium, Not A Transit Decarbonization Shortcut

Hydrogen buses can work, but the evidence shows a pathway rich in grants, announcements, and order claims while battery-electric buses scale.

Hydrogen buses have moved out of the brochure and into the depot. They have operated in Europe, North America, and Asia. They have accumulated pilot kilometres, city launches, funding awards, OEM announcements, national programme targets, and station openings. The technology is no longer a laboratory curiosity.

That is why it deserves a harder test. The procurement question is not whether a fuel-cell bus can complete a route. It can. The question is whether the full hydrogen bus operating system beats battery-electric buses once fuel supply, refueling stations, uptime, maintenance, warranties, emissions, and repeat procurement are counted.

This has been the through line in my hydrogen bus work for some time. I have written about failed hydrogen transit trials, hydrogen bus maintenance and fuel-cost problems, why transit agencies keep falling for hydrogen bus narratives, European hydrogen bus procurement reality, SunLine’s gray-hydrogen emissions and cost problem, Saarbahn’s €7.6 million refueling-station denominator, Vienna’s spare-parts warning, and Poland’s fuel-bill reality check. This review pulls those threads together as a transition pathway assessment.

Transit agencies do not buy technology symbols. They buy 12 to 15 years of service obligations. A bus that works on a demonstration route but brings an expensive fuel chain, fragile station dependency, thin maintenance ecosystem, and uncertain lifecycle emissions is not a shortcut. It is a risk premium with wheels.

Battery-electric buses are not magic either. Depot electrification takes planning. Grid connections can be slow. Routes need to be assessed. Charging windows matter. Cold weather matters. Maintenance practices change. Nobody serious should pretend that bus electrification is just a matter of dropping chargers onto a map and waiting for procurement magic to happen.

But hydrogen does not win by pointing at real battery-electric work and calling it a problem. Hydrogen has to beat the battery-electric pathway as it exists and as it keeps improving: depot charging, route scheduling, opportunity charging where needed, lower battery costs, growing OEM support, improving warranties, grid decarbonization, and the enormous advantage of using the electricity system instead of creating a new molecule supply chain for a small fleet class.

The evidence now points in one direction. Hydrogen buses remain technically real, but as a mainstream transit decarbonization pathway, they are defensive.

Verdict Summary

Pathway: Hydrogen fuel-cell buses for mainstream transit decarbonization

Verdict: Defensive, with narrow niche-valid cases

Confidence: High

Evidence quality: Strong for scale and activity-versus-progress assessment. Mixed for affordability and resilience. Incomplete for lifecycle emissions and full same-agency total cost of service.

Primary comparator: Battery-electric buses with depot charging, route scheduling, opportunity charging where needed, and continued grid decarbonization.

Update trigger: The verdict would change if multiple agencies made repeat lower-subsidy hydrogen-bus procurements after several years of operation, with transparent delivered hydrogen costs, station utilization, uptime, maintenance costs, availability, warranty terms, and lifecycle emissions comparable to or better than battery-electric bus systems.

What hydrogen buses claim to solve

The strongest case for hydrogen buses is straightforward. They offer zero tailpipe emissions, longer range, fast refueling, and less dependence on depot charging windows. Advocates also point to long blocks, cold-weather duty cycles, constrained depots, and weak grid connections. Governments add another claim, sometimes quietly and sometimes not: public buses can anchor a domestic hydrogen economy.

Some of those arguments are reasonable in constrained cases. A depot with serious grid limits, unusually long routes, short layovers, high daily kilometres, and existing access to cheap low-carbon hydrogen could find hydrogen buses useful. There are niches where battery-electric planning is harder. There are also jurisdictions where industrial policy will keep hydrogen buses alive because the bus is useful as a demand anchor for electrolyzers, fuel-cell suppliers, station operators, or domestic manufacturing.

That is not the same as a mainstream transit decarbonization pathway. “Could be made to work somewhere” is not the test. Engineers can make lots of things work with enough money, bespoke infrastructure, and patient public risk absorption. The professional question is whether the pathway works economically, repeatedly, maintainably, insurably, and at scale against alternatives that are also improving.

That is where the hydrogen bus case weakens. The vehicle is only the visible part. The pathway includes hydrogen production, compression or liquefaction, delivery, storage, dispensing, fuel quality, station maintenance, parts supply, technician capability, stack warranties, supplier durability, and decommissioning risk. A diesel bus plugs into a mature liquid-fuel system. A battery-electric bus extends the electricity system. A hydrogen bus asks a transit agency to stand up a specialized industrial gas supply chain for a fleet that is usually too small to carry the infrastructure efficiently.

That was the point of the hydrogen workshop transit agencies actually need. If an agency is determined to proceed with hydrogen buses, the workshop should not be a sales seminar about “zero emission” vehicles. It should be a risk workshop about delivered fuel costs, refueling station uptime, maintenance capability, fallback service, contract terms, fuel carbon intensity, and stranded infrastructure exposure.

That is a tall order. Sadly, no amount of ribbon-cutting makes kg per station per day go away.

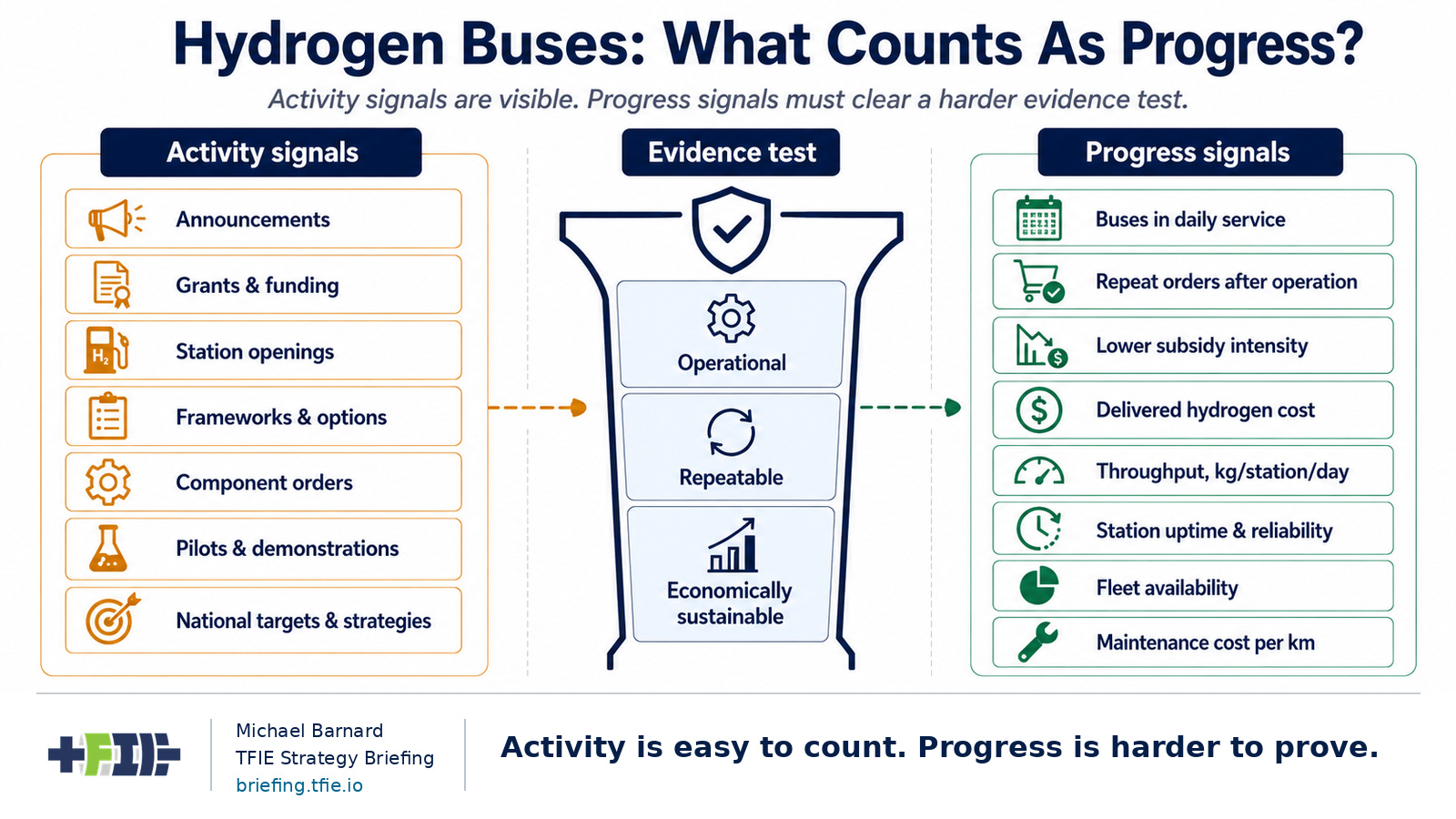

What is being counted as progress?

For this review, I assembled a public-source hydrogen bus procurement reality dataset using press releases, procurement records, funding sources, NREL reports, JIVE and JIVE2 material, station sources, market-denominator reports, and agency-level operating evidence where available.

The dataset is useful, but not because it produces a single heroic fleet total. A single heroic fleet total would be misleading. The useful result is that it shows how noisy the public evidence base remains.

A bus announcement is not a bus in service. A station opening is not station utilization. A grant is not durable demand. A framework agreement is not a firm fleet. An option is not an order. A component order is not an agency deployment. A pilot kilometre is not market formation.

Those distinctions sound pedantic until procurement decisions start writing cheques that the operating budget has to cash. Then they become the entire point.

The current workbook contains 273 source claims, 84 canonical fleet rows, 76 canonical procurement rows, and 20 open dedupe review items. Those numbers are not a global fleet count. They are an evidence map. They show how much public work is required just to separate what was announced from what was funded, what was ordered, what was delivered, what is actually operating, and what was later cancelled, paused, or reframed.

A cleanly scaling pathway should become easier to count over time. Buyers, deliveries, active fleets, operating costs, uptime, station utilization, and repeat orders should converge into a clearer record. Hydrogen buses still require a surprising amount of forensic separation between claims that proponents often want treated as equivalent.

This problem appears across hydrogen transport. In hydrogen transportation after HVS, I noted that hydrogen buses are the most visible surviving counterexample because real manufacturers, agencies, and governments are still active. But activity is not the same as durable market formation. The pattern across hydrogen transportation remains narrow niches, big subsidies, long pilots, and weak evidence that the pathway beats direct electrification at scale.

The main denominator reset is simple. Hydrogen buses should not be compared with diesel buses alone. They should be compared with battery-electric buses and depot charging. And the relevant denominator is not press releases, station announcements, or national targets. It is reliable service delivered at competitive cost and emissions, with transparent station utilization, repeat procurement, and declining subsidy dependence.

Hydrogen buses are real machines, not vaporware, but that is a low bar for transit procurement. The serious question is whether they survive contact with fleet-scale denominators: buses delivered versus buses actually in service, station utilization, delivered fuel cost, maintenance exposure, fleet availability, lifecycle emissions, warranty depth, and whether agencies come back for more after years of operation. That is the work below the paywall.