Grid Storage Through 2100: Batteries Lead, Pumped Hydro Anchors

A mostly electrified world needs roughly a hundred TWh of dedicated storage, with batteries leading and flexibility reducing what storage must solve.

Grid storage is no longer a speculative side issue in the energy transition. Batteries are scaling fast enough to reshape system planning, pumped hydro remains the durable bulk-storage anchor, and the long-duration storage category increasingly has to be separated into technologies with operating evidence and technologies still relying on claims that have not yet become repeatable fleets.

The harder question is not whether a mostly electrified world needs storage. Of course it does. The harder question is how much dedicated electrical storage is actually required once transmission, demand flexibility, seasonal thermal storage, strategic reserve and better system design are counted before the grid is forced to buy more batteries, more pumped hydro or another round of speculative storage.

This article is an update of my now years old 2100 base-case scenario, not a prediction. It tests what appears plausible if electrification continues, batteries keep scaling, pumped hydro remains the mature bulk-storage anchor, and flexibility, thermal storage, transmission and strategic reserve do their share of the work. I don’t claim to be right, I just claim to be less wrong than most, and being less wrong requires updating when deployment, costs and system thinking change.

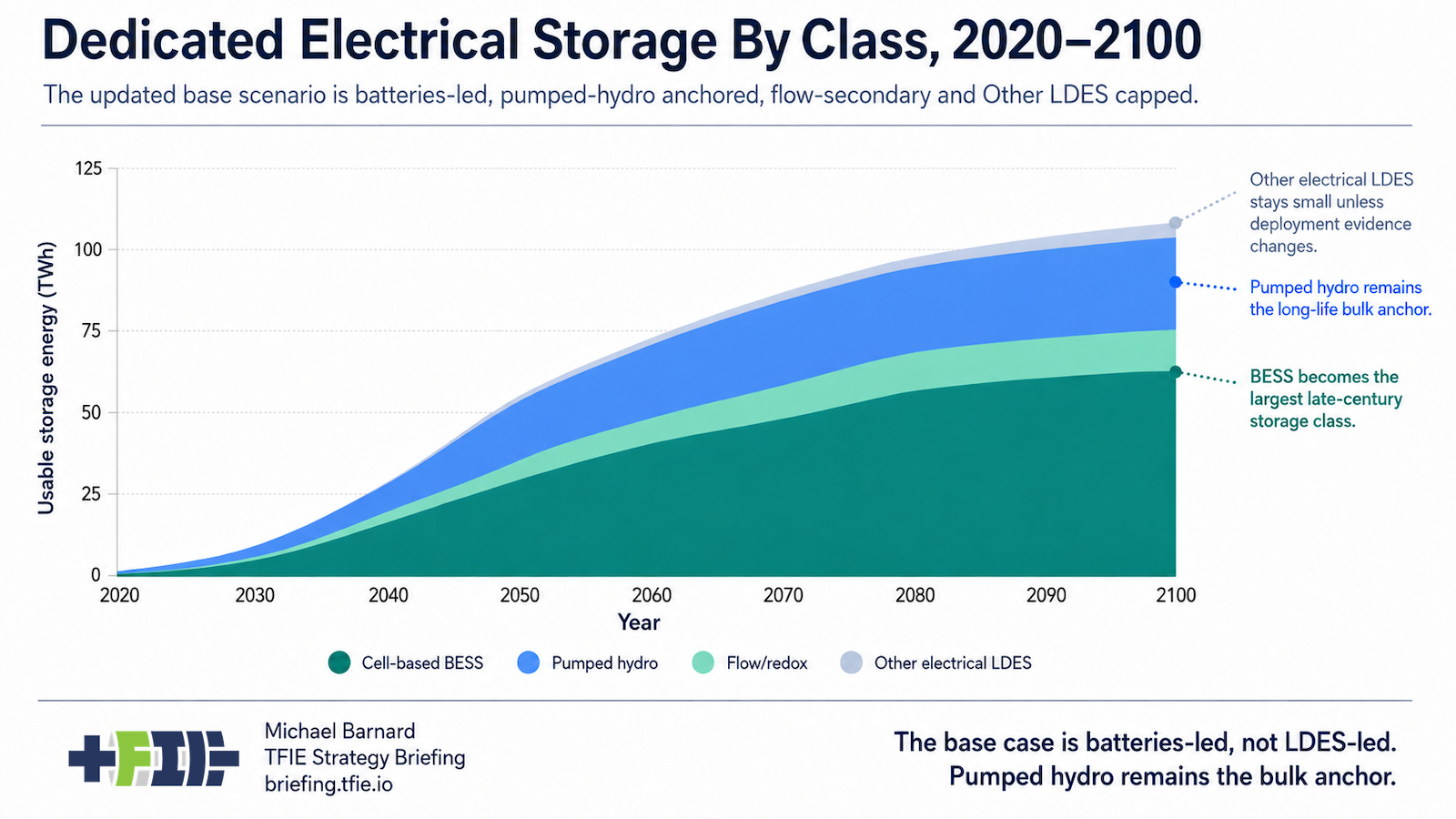

In my 2021 assessment of grid storage winners, the logic was pumped hydro first, lithium-ion for shorter-duration and ancillary-service work, and redox flow as the dark horse likely to gain share as storage duration lengthened. The projection that followed ran only to 2060, was framed mostly in GW rather than a full GW/TWh/duration stack, and used a rough read of Jacobson’s storage table to infer a much larger global energy requirement, around 210 TWh. Five years later, the parts that survived are the need for multiple storage classes, pumped hydro’s bulk-duration role, and the importance of not treating storage as a prerequisite for early renewable deployment. The parts that changed are the weights and the boundary: batteries have scaled faster and fallen further in cost than I expected, longer-duration BESS is now appearing in formal procurement, redox flow has not matched battery manufacturing scale or bankable deployment, and the model now separates dedicated electrical storage from V2X, demand flexibility, thermal storage, transmission and strategic reserve. The result is less flow, much more BESS, pumped hydro still large, Other electrical LDES still capped, and a lower dedicated-storage endpoint because the current model is not asking storage to solve every reliability problem.

The battery evidence is the first reason. The International Energy Agency reports that 108 GW of new battery storage was deployed globally in 2025, 40% more than in 2024, with installed capacity roughly eleven times higher than in 2021. That is not a demonstration market or a pre-commercial wave. It is infrastructure scaling at industrial speed, and any serious 2100 grid storage scenario has to treat batteries as the central manufactured storage technology.

The cost story pushes in the same direction. BloombergNEF’s 2025 battery price survey found stationary storage battery packs at $70/kWh, down 45% from 2024. Full battery systems still have inverters, containers, grid connections, civil works, fire systems and permitting to pay for, but the heart of stationary storage is now cheap enough to keep moving into duration bands that other technologies expected to own.

The old argument that batteries were for two and four hours while a broad long-duration storage category would own the rest is looking increasingly threadbare. The UK’s first LDES cap-and-floor minded-to portfolio includes multiple Li-ion BESS projects in the 8 to 18 hour range, which makes longer-duration BESS a formal procurement category rather than a speculative extension of today’s short-duration market. China sharpens the point: Rho Motion reported China’s BESS fleet at 106.9 GW / 240.3 GWh by May 2025, already larger in power-capacity terms than China’s reported end-2024 pumped-hydro fleet. The average duration is still only a bit over two hours, so this is not proof that 8 to 10 hour batteries have become the global norm, but it is a strong current signal that batteries are the fastest-scaling storage class.

Pumped hydro still matters enormously, and the projection preserves that. Pumped hydro is the gravity storage technology that actually works at grid scale, with mature equipment, long asset life and enough round-trip efficiency to be useful. China is the counterweight to any casual dismissal of pumped hydro. Reuters reported that China reached 58.69 GW of installed pumped storage by the end of 2024 after adding 7.75 GW that year, while the International Hydropower Association’s 2026 outlook says China now has 218 GW of pumped storage under construction.

But pumped hydro is a civil infrastructure project, not a factory product. It needs geology, water, transmission, permitting, revenue certainty, patient capital and political tolerance, while batteries need factories, containers, inverters and interconnection. Both are constrained, but they are constrained in different ways over a century-long scenario. The UK LDES portfolio shows the same role split at smaller scale: Li-ion batteries dominate project count, while pumped hydro carries most of the implied energy. The updated pathway therefore keeps pumped hydro as the long-life bulk anchor without pretending capital projects will outscale manufactured storage everywhere.

Flow batteries remain in the projection as a secondary medium-duration class. Flow batteries have real virtues, including stationary design, decoupled power and energy, potentially long cycle life and chemistries that may avoid some lithium-ion constraints. Grid storage, however, is won by repeat procurement, financeable warranties, delivered cost, bankable performance and operating fleets. Cheap batteries have narrowed the lane flow expected to occupy, so flow/redox remains material by 2100, but not co-dominant with batteries and pumped hydro.

The “Other electrical LDES” category is treated cautiously. Some ideas in that basket may find niches, but a base-case projection should not allocate tens of TWh to compressed air, liquid air, gravity blocks, iron-air, thermal-to-electric systems or other mechanisms simply because they claim the long-duration label. The UK’s first LDES support window does not change that treatment. It shows some diversity, including CAES and VFB/Zn, but the portfolio weight sits overwhelmingly with pumped hydro and Li-ion BESS. That is useful evidence of procurement interest, not evidence for letting “Other LDES” dominate a 2100 base case.

The updated base case lands at 108.5 TWh of dedicated electrical storage by 2100, but that number should not be read as a point prediction or as a figure borrowed from another model. It is a TFIE scenario anchor. The useful conclusion is that a mostly electrified world plausibly needs on the order of a hundred TWh of dedicated electrical storage, with batteries providing the largest share, pumped hydro providing the long-life bulk anchor, flow/redox providing a secondary medium-duration class and other electrical storage ideas remaining small until deployment evidence forces an update.

The public conclusion is straightforward. Batteries are now the strongest scaling signal. Pumped hydro remains the best large physical storage asset. Flow batteries retain a narrower but still material role. Other LDES has to earn its way into the model with operating fleets, not announcements or category claims. The updated pathway is not batteries-only, but it is batteries-led, and the rest of the reliability stack matters because storage should not be forced to solve problems that flexibility, heat, transmission and strategic reserve solve better.

Below the paywall is the professional layer: the storage boundary, provenance of the 108.5 TWh and 9.2 TW scenario anchors, comparison with full-electrification and renewables studies, the UK and China evidence signals, system-lever treatment, update triggers, decision implications and scorecard I’ll use to judge whether grid storage technologies are scaling, progressing, niche-valid, stalled or still not demonstrated at fleet scale.